Accruals and deferrals involve adjusting entries to record transactions that have occurred but have not yet been recorded. Reclassifications involve moving amounts between accounts, while estimates involve adjusting amounts based on expected future events. Adjustment entries can also impact a business’s profitability by affecting the amount of revenue and expenses that are recorded what are dilutive securities dilutive securities meaning and definition in a particular accounting period. For example, if an adjustment entry is made to increase revenue, this will increase the business’s profitability for that period. Conversely, if an adjustment entry is made to increase expenses, this will decrease the business’s profitability for that period. Depreciation is the allocation of the cost of a long-term asset over its useful life.

Accrual Accounting and Adjusting Journal Entries

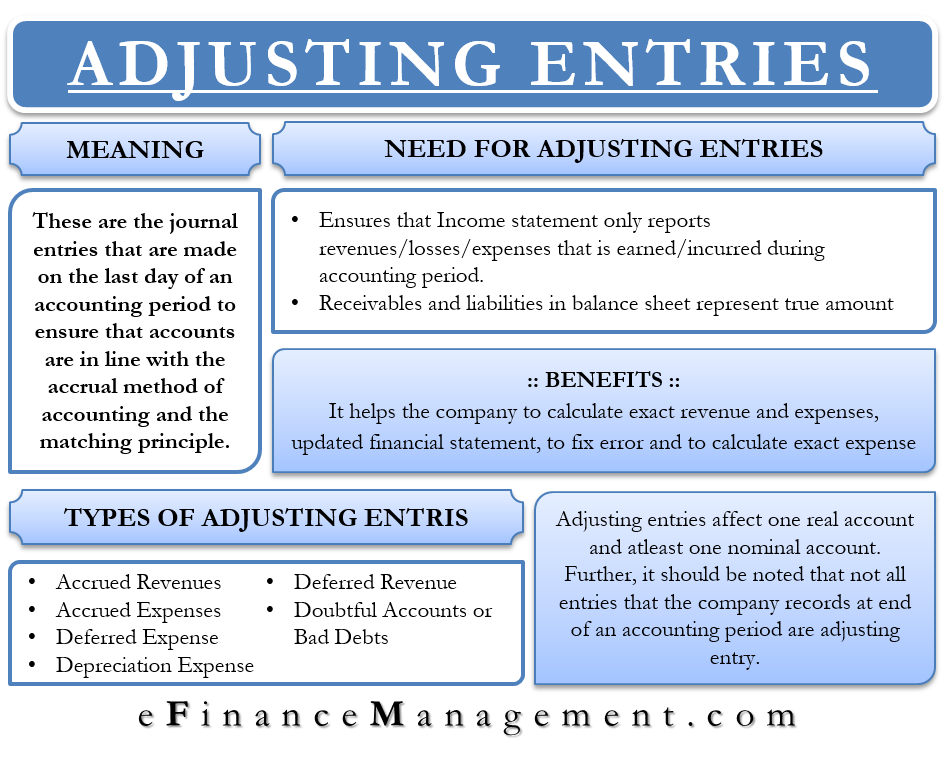

Adjusting Entries reflect the difference between the income earned on Accrual Basis and that earned on cash basis. This enables us to arrive at the true result of business activities for a given period (e.G., Whether we made profits or suffered losses). One of the most common mistakes is making incorrect accounting entries. This can happen due to a lack of attention to detail or a misunderstanding of accounting principles.

What are the 4 types of adjustments in accounting?

- If you have a bookkeeper, you don’t need to worry about making your own adjusting entries, or referring to them while preparing financial statements.

- The financialstatements must remain up to date, so an adjusting entry is neededduring the month to show salaries previously unrecorded and unpaidat the end of the month.

- The entry records any unrecognized income or expenses for the accounting period, such as when a transaction starts in one accounting period and ends in a later period.

- It also helps users (lenders, employees and other stakeholders) to assess a business’s financial performance, financial position and ability to generate future Cash Flows.

- The following entries show theinitial payment for the policy and the subsequent adjusting entryfor one month of insurance usage.

- Under the cash method of accounting, a business records an expense when it pays a bill and revenue when it receives cash.

These entries are made at the end of an accounting period to update accounts that were not properly recorded during the period. Adjustment entries are important accounting tools that help businesses to accurately record their financial transactions and ensure that their financial statements are accurate. These entries are made at the end of an accounting period to adjust the accounts to their correct balances. Deferred revenue is revenue that has been received but not yet earned.

What is your current financial priority?

Accounting software can be used to simplify the process of recording adjustment entries. Most accounting software has built-in features that allow for the easy creation and recording of adjustment entries. To begin, the bookkeeper or accountant must identify the need for an adjustment entry. This could be due to an error in the original journal entry, the need to accrue expenses or revenue, or the need to record depreciation. The revenue recognition principle requires businesses to recognize revenue when it is earned, regardless of when payment is received.

Interest expense arises from notes payable and other loanagreements. The company has accumulated interest during the periodbut has not recorded or paid the amount. You cover more detailsabout computing interest in Current Liabilities, so for now amounts are given. Accrued expenses are expenses incurred in aperiod but have yet to be recorded, and no money has been paid.Some examples include interest, tax, and salary expenses.

Accounting 101: Adjusting Journal Entries

Such receipt of cash is recorded by debiting the cash account and crediting a liability account known as unearned revenue. At the end of the accounting period, the unearned revenue is converted into earned revenue by making an adjusting entry for the value of goods or services provided during the period. Recording transactions in your accounting software isn’t always enough to keep your records accurate. If you use accrual accounting, your accountant must also enter adjusting journal entries to keep your books in compliance.

In all the examples in this article, we shall assume that the adjusting entries are made at the end of each month. Did we continue to follow the rules of adjusting entries inthese two examples? In this case, Unearned Fee Revenue increases (credit) and Cashincreases (debit) for $48,000.

Therefore, it is necessary to find out the transactions relating to the current accounting period that have not been recorded so far or which have been entered but incompletely or incorrectly. An adjusting entry is an entry that brings the balance of an account up to date. Adjusting entries are crucial to ensure the correct balance and correct information in an account at the end of an accounting period. Adjustment entries can impact a business’s cash flow by affecting the timing of cash inflows and outflows. For example, if an adjustment entry is made to increase accounts receivable, this will increase the amount of cash that the business expects to receive in the future. On the other hand, if an adjustment entry is made to increase accounts payable, this will decrease the amount of cash that the business expects to pay in the future.

To make an adjusting entry for wages paid to an employee at the end of an accounting period, an adjusting journal entry will debit wages expense and credit wages payable. Adjusting entries must involve two or more accounts and one of those accounts will be a balance sheet account and the other account will be an income statement account. You must calculate the amounts for the adjusting entries and designate which account will be debited and which will be credited. Once you have completed the adjusting entries in all the appropriate accounts, you must enter them into your company’s general ledger. Adjustment entries are an important part of the accounting process that ensures financial statements are accurate and reflect the true financial position of a company.

For example, a company performs landscaping services in theamount of $1,500. Atthe period end, the company would record the following adjustingentry. Interest Receivable increases (debit) for $1,250 becauseinterest has not yet been paid. Interest Revenue increases (credit)for $1,250 because interest was earned in the three-month periodbut had been previously unrecorded. For example, let’s say a company pays $2,000 for equipment thatis supposed to last four years. The company wants to depreciate theasset over those four years equally.